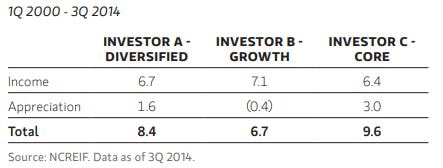

Core & Secondary Market Scenario Analysis

We took 10 highly liquid markets that have traditionally been popular with institutional investors.13 We then imagined that three investors were each building an office portfolio. The investors would allocate an equal amount to each of the office markets they selected and buy their entire portfolio in the first quarter of 2000. Investor A believes in having a well-diversified portfolio that includes both primary and secondary markets. Investor A, therefore, invests 10 percent of her portfolio in each of the 10 markets. Investor B prefers high cap rate secondary markets and, instead, limits his portfolio to five markets, allocating 20 percent to Dallas, Houston, Phoenix, Chicago and Atlanta.

Finally, Investor C insists on investing only in primary markets that exhibit supply constraints. Investor C purchases office buildings in Washington, DC, New York, Boston, San Francisco, Seattle and Los Angeles.

We believe today’s historically low volatility will eventually come to an end. When it does, appreciation gains will cease to be driven by cap rate compression, and instead will rely entirely on NOI growth (which has historically been the main driver of asset appreciation). Thus, with expectations of NOI growth becoming increasingly important to core real estate returns, we would prefer to stick with markets that have a strong historical tendency to appreciate instead of attempting to play the market timing game.

Acore investor’s journey is a long one that will undoubtedly require them to sail through an economic storm or two. We, therefore, reiterate that core investors should resist the temptation of the Sirens’ song to “chase yield into secondary markets.” We have already seen how this plays out, shipwrecked on the rocks. Instead, as we have shown, core investors should stay the course and chase appreciation—this has historically been the best way to protect capital and realize long term outperformance. The definition of a core market should not change with the whims and perceptions of market participants. Rather, core markets are characterized by three structural traits: liquidity, market depth and supply constraints. To chase yields in secondary markets by expanding one’s definition of core has historically been a poor strategy. Instead, it is when market discipline is declining (and leading participants into secondary markets) that one should be most wary of deviating from strategy.

Liquidity, Market Depth and Supply

Liquidity = transaction volume (SF) / inventory (SF)

A core investor should consider is market liquidity, or how easily they can exit the market. When evaluating liquidity for a given market, core investors should stick to the markets that see high liquidity in both good times and bad.

Market Depth

Second, investors should consider how “deep the bench is” in a given market. A deep bench of potential tenants provides a core investor with some protection against significant re-leasing risk in the event a major tenant vacates. To evaluate the depth of each market, we looked at the average absorption rate in relation to market size.

It's all about Supply

In our view, supply is the greatest long term risk to appreciation, and, therefore, our final criterion is that the market has supply constraints. While supply is responsive to increases in tenant demand, it is generally unresponsive to market declines. Thus, since excess supply is not eliminated from the market, rents must fall as landlords compete to fill their space. Moreover, by favoring markets with low average vacancies, we focus only on office markets that will generally give an edge to landlords to push rents and grow NOI.

A core investor should consider is market liquidity, or how easily they can exit the market. When evaluating liquidity for a given market, core investors should stick to the markets that see high liquidity in both good times and bad.

Market Depth

Second, investors should consider how “deep the bench is” in a given market. A deep bench of potential tenants provides a core investor with some protection against significant re-leasing risk in the event a major tenant vacates. To evaluate the depth of each market, we looked at the average absorption rate in relation to market size.

It's all about Supply

In our view, supply is the greatest long term risk to appreciation, and, therefore, our final criterion is that the market has supply constraints. While supply is responsive to increases in tenant demand, it is generally unresponsive to market declines. Thus, since excess supply is not eliminated from the market, rents must fall as landlords compete to fill their space. Moreover, by favoring markets with low average vacancies, we focus only on office markets that will generally give an edge to landlords to push rents and grow NOI.

Physical and Financial Cycle affect Real Estate Cycle

The performance of the real estate market is affected by changes in physical and financial cycles. Real estate cycles typically last over a decade, and reflect a process of events

such as fluctuating prices, vacancies, and rental demand.

>The physical cycle represents vacancy rates which, in turn, influence changes in rental levels.

>The financial cycle represents the capital flows that go towards funding real estate developments; new construction affects the price of real estate.

such as fluctuating prices, vacancies, and rental demand.

>The physical cycle represents vacancy rates which, in turn, influence changes in rental levels.

>The financial cycle represents the capital flows that go towards funding real estate developments; new construction affects the price of real estate.

Family Office Long-term Strategies

Managers seeking commitments from family offices may find more success by emphasizing their high level of due diligence and putting effort into building long-term relationships.

Multifamily residential was the most attractive property type for 2019, with 77.7 percent of families indicating interest, likely because the investment strategy is one that is easy to understand, Industrial properties and hotels followed, with 38.8 percent and 27.7 percent showing interest, respectively. In that regard, “family offices are more like retail investors than institutional investors,”

The outcome of family investments was often considered personal, with 76.4 percent of respondents saying they want to use real estate to create generational wealth.

Multifamily residential was the most attractive property type for 2019, with 77.7 percent of families indicating interest, likely because the investment strategy is one that is easy to understand, Industrial properties and hotels followed, with 38.8 percent and 27.7 percent showing interest, respectively. In that regard, “family offices are more like retail investors than institutional investors,”

The outcome of family investments was often considered personal, with 76.4 percent of respondents saying they want to use real estate to create generational wealth.

CRE Lender judge quality of property by 2 basic criteria

1. many different tenants can use the property

2. the property can be leased or managed by different owners

2. the property can be leased or managed by different owners

Correlation Coefficient - Types & Geography

Over the last 23 years, the correlation coefficient between government bonds and both of these real estate portfolios is nearly zero. The conclusion is that a globally diversified real estate portfolio was little related to the US interest rate cycle.

Cross-border correlation remains low, fund that are big enough to exploit these low correlation can produce greater portfolio resilience. "Global diversification" has historically offered even more resilience benefits than "sector allocation" up from.

Cross-border correlation remains low, fund that are big enough to exploit these low correlation can produce greater portfolio resilience. "Global diversification" has historically offered even more resilience benefits than "sector allocation" up from.

Strategy on Asset, Disposition Operation enhancement

-Asset improvement strategies through renovations, rebranding, and resident services.

-Operational enhancements through strategic planning, revenue enhancement, expense control, and performance monitoring and reporting.

-Disposition strategies through regular hold-sell analysis and continuous dialogue with our network of buyers.

-Operational enhancements through strategic planning, revenue enhancement, expense control, and performance monitoring and reporting.

-Disposition strategies through regular hold-sell analysis and continuous dialogue with our network of buyers.

Service Apartment or Hotel in late Cycle?

In good times it is possible to maximize margins with serviced apartments because of the ability to adjust inventory based on shifting demand. In addition, there is a lower risk involved with the segment because revenue is not as variable as with a hotel.

The variability in the performance of serviced apartments is far less volatile than hotel or extended stay because operators can vary supply depending on demand.

The variability in the performance of serviced apartments is far less volatile than hotel or extended stay because operators can vary supply depending on demand.

Classify Global real estate markets

In addition to a geographic distinction of markets, we can also classify them based on the business sector, which is a key driver of demand for commercial space. For instance, markets can be distinguished by whether they are mainly driven by commodities, finance, or government sector. The first category includes cities such as Brisbane, Perth, Calgary, and Santiago de Chile. Markets that largely depend on the financial industry are typically London, New York, and Tokyo, while the commercial real estate demand in cities like Berlin and Washington D.C. depends stronger on the public sector.

Medical Office - Long-term trend

Aging Population to Support Medical Office Demand - The population of people over age 65 is expected to nearly double between 2015 and 2055, which is an encouraging factor supporting long-term demand for medical office

*Phoenix, for instance, is forecast to gain 11.9 percent in overall population, but 29.4 percent in the over-65 set between now and 2021. Other strong elderly population gainers are Las Vegas, South Florida, Atlanta and Dallas/Ft. Worth—all more than 25 percent by 2021.

*Phoenix, for instance, is forecast to gain 11.9 percent in overall population, but 29.4 percent in the over-65 set between now and 2021. Other strong elderly population gainers are Las Vegas, South Florida, Atlanta and Dallas/Ft. Worth—all more than 25 percent by 2021.

Selected U.S. Vacation Rental Property Areas - Updating

Branson, MO Carlsbad, CA

Galveston, TX Lake Gregory, CA

Biloxi, MS Cayucos, CA

Lake Arrowhead, CA Lake Norman, NC

Kissimmee, FL Dillon, CO

Poconos, PA Lynchburg, VA

Galveston, TX Lake Gregory, CA

Biloxi, MS Cayucos, CA

Lake Arrowhead, CA Lake Norman, NC

Kissimmee, FL Dillon, CO

Poconos, PA Lynchburg, VA

Risks specific to real estate investing

Sector risk

There are a number of factors which may affect the real estate sector, including the cyclical nature of real estate values, over-development and increased competition, increases in real estate taxes and operating expenses, demographic trends and variations in rental income. Changes in the appeal of properties to tenants, increases in interest rates, the level of gearing in the real estate market and other real estate capital market influences can also affect the performance of the sector.

Vacancy risk

The risk of a tenant vacating a property, failing to meet their rental obligations or failing to renew a lease can have a detrimental impact on rental returns.

Value risk

Asset values are influenced by location, supply and demand, rental agreements, occupancy levels, obsolescence, tenant covenants, environmental issues and government or planning regulations. Changes to these drivers may affect the end value of the asset. A good approach for those wishing to minimize risk is to invest in real estate which is leased to good quality corporate type tenants. In selecting assets, we believe the higher the quality of the asset, the higher the quality of the tenant. Therefore, it is advisable to look for well-located properties, in locations such as central business districts or central shopping malls, with lengthy and secure income streams.

There are a number of factors which may affect the real estate sector, including the cyclical nature of real estate values, over-development and increased competition, increases in real estate taxes and operating expenses, demographic trends and variations in rental income. Changes in the appeal of properties to tenants, increases in interest rates, the level of gearing in the real estate market and other real estate capital market influences can also affect the performance of the sector.

Vacancy risk

The risk of a tenant vacating a property, failing to meet their rental obligations or failing to renew a lease can have a detrimental impact on rental returns.

Value risk

Asset values are influenced by location, supply and demand, rental agreements, occupancy levels, obsolescence, tenant covenants, environmental issues and government or planning regulations. Changes to these drivers may affect the end value of the asset. A good approach for those wishing to minimize risk is to invest in real estate which is leased to good quality corporate type tenants. In selecting assets, we believe the higher the quality of the asset, the higher the quality of the tenant. Therefore, it is advisable to look for well-located properties, in locations such as central business districts or central shopping malls, with lengthy and secure income streams.

Cap rates are influenced by

-The rate of return on the 10 year Treasury Bill

-The availability of debt in the market (the more debt, the lower the cap rates)

-The overall health of the real estate market

-The rent roll of the property (tenant quality, lease terms, etc.)

-The availability of debt in the market (the more debt, the lower the cap rates)

-The overall health of the real estate market

-The rent roll of the property (tenant quality, lease terms, etc.)